The 1st July deadline has arrived, what should real estate agencies do next?

Preparing for AML/CTF was only the first step. Learn how to keep your agency compliant with practical tips on due diligence, ongoing training, risk assessments and everyday processes.

For months, the real estate industry has been preparing for 1st July.

Policies were written.

Teams completed training.

Compliance officers were appointed.

Technology was implemented.

Agencies enrolled with AUSTRAC.

For many businesses, getting ready for the deadline became a major project.

Now the deadline has arrived.

So… what happens next?

This is where the real work begins.

Because being compliant isn’t the finish line.

It’s the point where AML/CTF becomes part of your agency’s everyday routine.

Compliance needs to become part of the way your agency works

Getting everything ready before 1st July was a huge achievement.

Keeping those processes alive is the bigger challenge.

It’s one thing to have an AML/CTF program sitting in a folder.

It’s another to have your whole team confidently following it every day.

That means making sure everyone understands:

- When customer due diligence needs to happen

- When risk assessments should be completed

- What red flags to look for

- What your internal processes are

The first few weeks will probably involve plenty of questions.

“Do I verify this client now?”

“Does this trigger a risk assessment?”

“Have we completed everything before providing the service?”

That’s completely normal.

Like any new process, confidence comes with repetition.

Keep the conversation going

One training session isn’t enough.

AML/CTF shouldn’t become something the team only talks about once a year.

Regular refreshers, team discussions, and practical examples help everyone stay aligned, especially while the legislation is still new.

Every agency will develop its own rhythm.

The important thing is making compliance part of everyday conversations, not something people only remember when they’re completing paperwork.

Don’t make exceptions because you know the client

This is probably one of the biggest misconceptions.

You’ve worked with the vendor before.

They’re a long-term client.

You know them personally.

Surely, they don’t need to be verified again?

They absolutely do.

Your relationship with the client doesn’t replace your obligations under the legislation.

Customer due diligence applies regardless of how well you know someone.

For vendors, those checks need to be completed before you begin providing a designated service.

In many cases, that means after they’ve signed the authority to act, but before the property goes live.

It’s also worth remembering that due diligence is much more than checking a driver’s licence.

Depending on the circumstances, it may include:

- Identity verification

- Politically exposed persons (PEP) screening

- Sanctions screening

- Adverse media checks

- Risk assessments

Having the right technology in place can make these checks much quicker, but they still need to happen.

Remember why these obligations exist

It’s easy to think about AML/CTF as another compliance requirement.

A few more forms.

Another process.

Another box to tick.

The purpose is much bigger than that.

Real estate professionals are in a unique position.

You’re often one of the first people involved in a property transaction.

That makes agents an important line of defence against financial crime.

Money laundering often relies on moving illicit funds through legitimate transactions.

Property has long been recognised as one avenue criminals may attempt to use.

By identifying unusual behaviour, completing customer due diligence, and reporting suspicious activity where required, agencies play an important role in protecting Australia’s financial system.

Sometimes it’s helpful to remember the reason behind the process.

Technology should reduce effort, not responsibility

Digital verification platforms have made AML/CTF much easier to manage.

Identity verification.

PEP screening.

Sanctions checks.

Adverse media screening.

Risk assessments.

Many of these tasks can now be completed in minutes instead of manually searching across multiple sources.

That’s a huge step forward.

But technology doesn’t replace professional judgement.

Agencies are still responsible for understanding their obligations, recognising suspicious activity, and making sure their policies are being followed consistently.

The best compliance technology feels built into your workflow, not bolted onto it.

It reduces effort.

It doesn’t remove responsibility.

The deadline has arrived, but the learning doesn’t stop here

For many agencies, the hard work of preparing for 1st July is complete.

The focus now shifts to making AML/CTF part of everyday business. Building confidence across your team, following your processes consistently, and making sure compliance becomes part of the way your agency works.

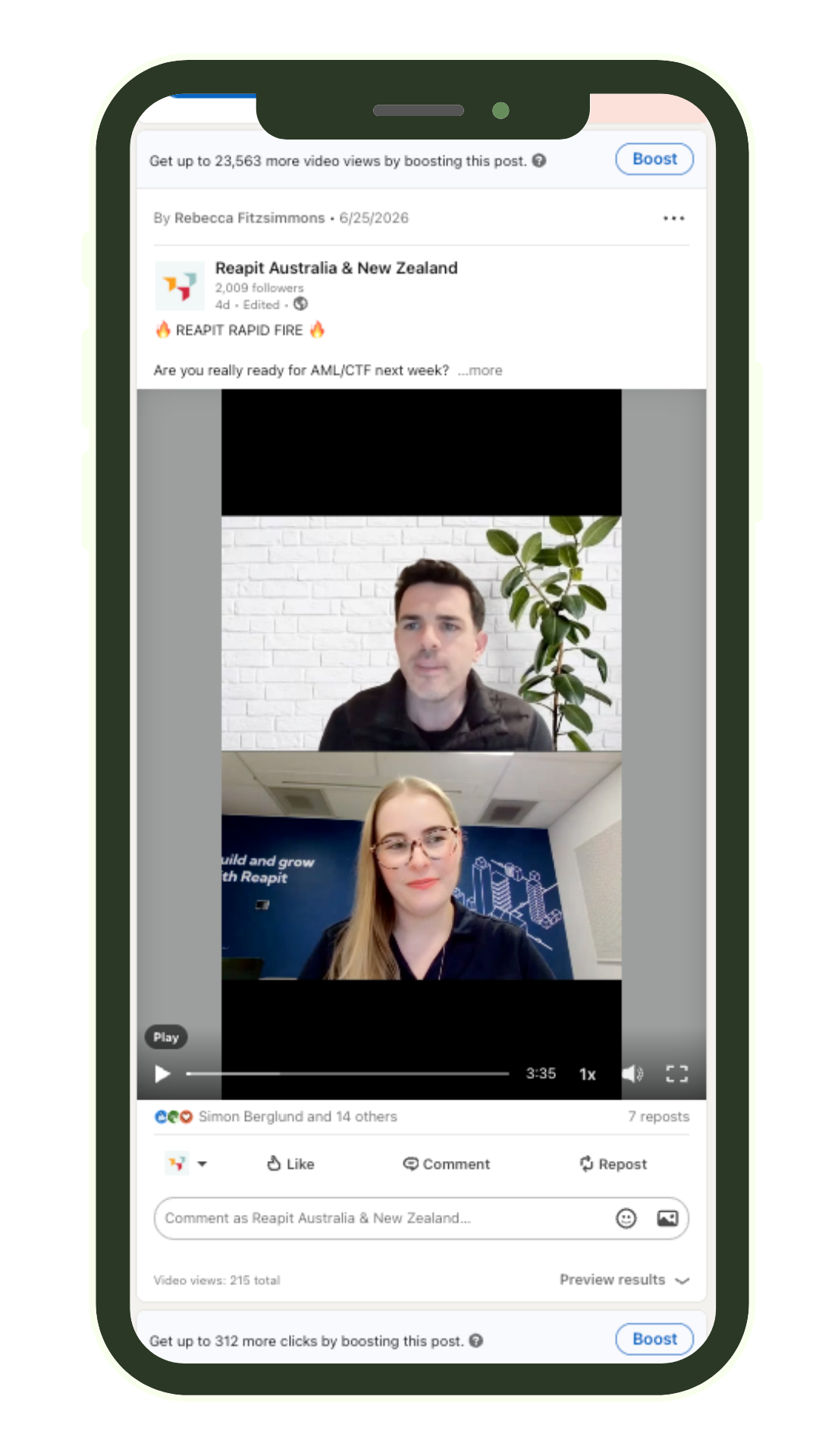

If you’re looking for practical advice, watch our recent Rapid Fire conversation with Alana De Gee (Head of Transactional Revenue), where she answers some of the most common questions agencies are asking now that legislation is in effect, including what happens after 1st July, why customer due diligence matters, and the role agents play in helping prevent financial crime.

And if you’d like to dive deeper, we’ve also put together a Reapit Verify Webinar Series:

Learn more about Reapit Verify here.

Whether you’re still refining your processes or looking to simplify compliance, the goal remains the same: make AML/CTF part of the way your agency operates.

The deadline may have been 1stJuly.

Building confident, consistent compliance is what comes next.

.jpeg)